Private equity (PE) remains one of the most dynamic and influential forces in global capital markets. From fueling innovation in fast-growing startups to transforming legacy corporations, PE firms employ a range of investment strategies tailored to different company stages, market conditions, and risk profiles. Among these, three categories dominate the landscape: Add-On Acquisitions, Leveraged Buyouts (LBOs), and Growth Equity.

Each of these investment profiles serves a distinct purpose in the private capital ecosystem. Understanding how they differ is crucial for fund managers, LPs, and entrepreneurs navigating today’s complex investment environment. Below, we explore each strategy in detail, supported by academic research and the latest market trends.

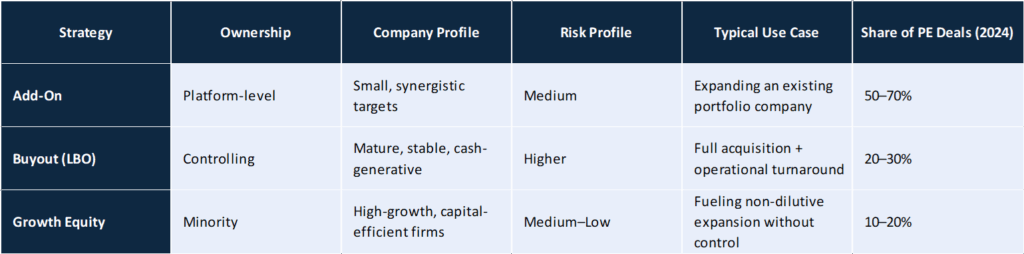

Add-On Acquisitions: Building Value Through Strategic Expansion

In recent years, add-on acquisitions have emerged as the most common private equity deal type, especially in North America. These transactions involve the acquisition of smaller, often privately held businesses that are integrated into an existing portfolio company, known as a platform. The objective is to scale operations, enter new markets, or consolidate fragmented sectors.

According to Bain & Company’s Global Private Equity Report 2024, add-ons made up over 70% of buyout transactions in the U.S., reflecting the growing emphasis on buy-and-build strategies. Industries like healthcare, IT services, and specialty manufacturing are particularly ripe for this model due to their high fragmentation and recurring revenues.

Academic studies support the effectiveness of this approach. Research from Hammer, Knauer, and Pflueger (Harvard Business School, 2017) found that platform companies executing multiple add-ons tend to experience faster revenue growth, higher exit multiples, and more efficient capital deployment. These benefits stem from operational synergies, cross-selling opportunities, and the ability to acquire at a discount to the platform’s valuation.

Add-ons are also attractive because they generally require less upfront capital and involve lower execution risk. For PE firms looking to compound value efficiently, they offer a powerful lever to drive EBITDA growth without relying on macroeconomic tailwinds.

Leveraged Buyouts: The Cornerstone of Control-Oriented Private Equity

The leveraged buyout (LBO) remains the most recognisable and foundational strategy in private equity. In an LBO, the PE firm acquires a controlling or full ownership stake in a company, using a substantial amount of debt to finance the acquisition. The goal is to enhance the business’s operational performance and return it to the market — either through a sale or IPO — at a significantly higher valuation.

Despite higher interest rates in 2023–2024, the LBO market has shown signs of resilience. PitchBook data reveals that buyouts accounted for roughly 26% of global PE transactions in 2024, with Europe leading the recovery through corporate carve-outs and take-private transactions.

A widely cited academic analysis by Kaplan and Strömberg (2009) illustrates how LBOs generate value through a combination of operational improvements, tight cost control, governance enhancements, and debt optimisation. Their findings show that, when executed well, LBOs often outperform public equities over the investment cycle, particularly during periods of moderate credit availability and stable inflation.

In today’s more cautious credit environment, PE firms are adapting by focusing less on leverage and more on operational alpha, targeting businesses with improvement potential in pricing, supply chain efficiency, and digital transformation. This signals a return to fundamentals, where hands-on management and sector expertise drive returns.

Growth Equity: Capital Without Control, Acceleration Without Dilution

At the intersection of venture capital and buyouts lies growth equity, a strategy that provides minority capital to fast-growing companies with proven business models. Unlike LBOs, growth equity investors do not seek control. Instead, they partner with founders and management teams to fuel expansion, product development, or market entry without disrupting governance structures.

Preqin reports that growth equity investments accounted for 18% of global PE activity in 2024, with a strong tilt toward technology, fintech, and healthcare sectors. In Asia and emerging markets, growth equity has become a preferred alternative to venture capital, particularly for companies approaching IPO readiness.

From an academic perspective, Gompers and Kaplan (2015) highlight that growth equity offers a compelling risk-reward profile. Their research shows that companies receiving such investments typically demonstrate strong revenue compounding, and growth investors benefit from valuation uplift at exit, often via strategic sale or public offering. Importantly, this strategy avoids the binary risk of early-stage VC while maintaining access to high upside.

Growth equity is particularly relevant in today’s environment, where many private companies are staying private longer. By offering flexible capital with strategic input, growth equity fills a critical financing gap — and does so with lower dilution and operational disruption.

Final Thoughts

While these three strategies differ in structure, they all reflect the evolution of private equity from a niche financial tool to a mainstream engine of business transformation. Add-ons focus on compounding through scale, buyouts target control and restructuring, and growth equity offers capital to accelerate momentum.

For investors and founders alike, understanding these models is key to aligning with the right capital at the right stage. As the PE landscape grows more competitive, the firms that master multiple strategies — and adapt them to market realities — will be the ones that continue to deliver outsized returns in the decade ahead.