REITs (Real Estate Investment Trusts) offer investors an attractive combination of income, diversification, and potential capital appreciation. As of the end of 2024 and the start of 2025, many REITs are trading at multiples significantly lower than historical averages.

Valuations approached very attractive levels, though the picture varies across sectors due to the unique nature of their underlying assets, tenant profiles, lease structures, and sensitivity to economic trends. Each sector’s valuation reflects its unique balance of risk and reward. For example, sectors like industrial and speciality REITs may offer attractive valuations due to strong growth prospects and stable cash flows. In contrast, office and retail REITs might face more headwinds from changing market dynamics, leading to more conservative valuations. Depending on the classification, equity REITs can be divided into roughly 10 sectors with a very different riks-returns profile and wide return deviation in any given year. Nearly half of the market cap of publicly traded REITs falls into 3 sectors: Industrial REITs (19.2%), retail REITs (17.9%), and multifamily residential REITs (10.4%).

Investors need to assess these sector-specific factors. This article looks at the overall REITs picture and the investment opportunity they offer in 2025.

Attractive Valuations

REIT multiples are currently at multi-decade discounts, allowing investors to pay less for each unit of cash flow than historical averages would suggest. In simple terms, valuation multiples—such as the FFO (Funds From Operations) multiple—reflect the price investors are willing to pay relative to the cash flows generated by a REIT’s portfolio. For example, NNN RETI Inc. is trading at approximately 12x FFO, compared to its historical average of 18x, while Crown Castle Inc. is trading at 14.5x FFO, well below its long-term norm.

Since the end of 2021, as monetary policies became more restrictive, investors have been forced to discount future cash flows, resulting in lower valuation multiples. In addition, short-term headwinds—such as lease cancellations, increased variable debt costs, and suboptimal capital allocation—have contributed to a pessimistic market outlook. However, these issues are primarily transitory and do not reflect the underlying long-term fundamentals of REITs.

The expectation is that as restrictive monetary policies ease and inflation pressures subside, market sentiment will improve, leading to a multiple expansion. These lower multiples represent a margin of safety, meaning investors pay less relative to the underlying cash flows, creating an attractive risk-reward profile.

Margin of safety

REIT asset valuations, typically disclosed in quarterly reports or available through third-party platforms, are usually audited as part of a REIT’s financial reporting. The discount to NAV is the percentage difference between a REIT’s estimated net asset value per share and its current market price—with some REITs currently trading at discounts as steep as 30-40%. This significant discount acts as a buffer against valuation errors or market downturns, providing a margin of safety for investors if underlying property values are overestimated or market conditions worsen. However, investors should remain cautious because NAV figures depend on property valuations that involve subjective estimates.

High Yield

The average dividend yield on U.S. REITs is about twice that of the S&P 500, and some REITs pay even higher dividends. In fact, with 29 REITs among the 500 S&P companies, their inclusion boosts the overall index yield. Compared to the broader equity market—often characterized by higher volatility and inflated valuations—REITs offer a more stable income stream through attractive yields and consistent cash flows. For example, REITs like Realty Income, NNN Reit, ARE, and WP Carey provide 5–7% yields with defensive business models. With upcoming lease renegotiations and rental adjustments to market rates, these REITs offer sustainable dividends and hold the potential for income growth.

Defensive characteristic

REITs that utilize triple net leases transfer most operating expenses—such as taxes, insurance, and maintenance—to their tenants, reducing financial risk and enhancing stability. With these leases often featuring annual rent escalations of 1.5–2%, they ensure that rental income steadily increases over time, even in challenging economic conditions. Furthermore, many of these REITs boast robust balance sheets and maintain relatively low leverage, which positions them to benefit from potential declines in interest rates. Together, these factors contribute to the defensive characteristics of such REITs, offering investors a more predictable and resilient income stream during economic downturns.

Tactical allocation in the current backdrop

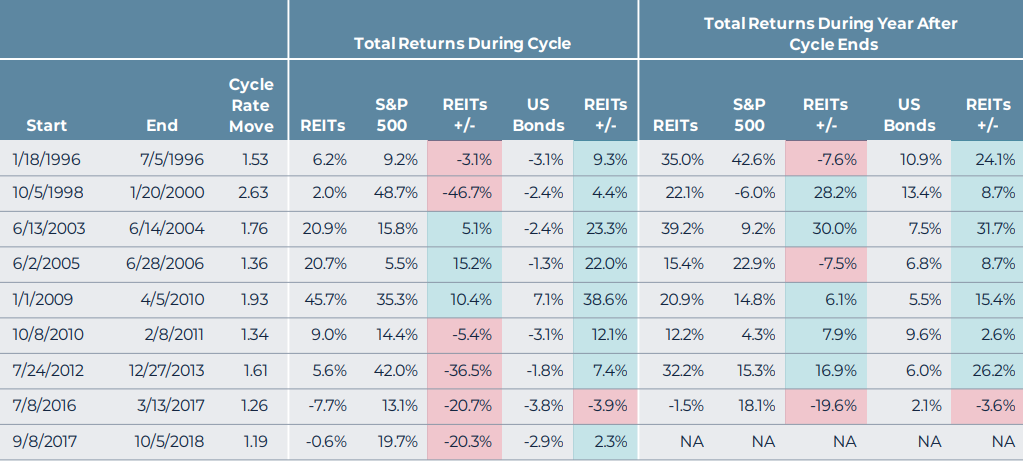

Research indicates that REITs typically maintain positive performance even when interest rates are rising. During these periods, they significantly outperform bonds, though they generally underperform the S&P 500. However, following episodes of rising yields, REITs almost always deliver positive returns, outperforming bonds and, most of the time, the S&P 500. This resilience is partly due to their sensitivity to interest rate changes, as REITs rely heavily on debt to finance property acquisitions and development.

Performance During and After 10 Year Treasury Yield Upcycles

Source: AEW ‘Rising Interest Rates and REITs’, based on Factset, S&P, Bloomberg Barclays, and MSCI data.

With the Federal Reserve and other central banks poised to exit the rate-hiking cycle—a period that historically has driven up discount rates on future cash flows and compressed REIT valuations, as seen during the mid-2000s—there is an optimistic outlook. If inflation pressures ease and monetary policy returns to normal, there is considerable potential for dividend growth and capital appreciation, which would boost overall risk-adjusted returns.

Notably, during times when both economic growth and yields declined, U.S. REITs delivered an average annualized return of 19.5%.

Risk premium

Studies consistently show that equity REITs have historically offered dividend yields that exceed U.S. Treasury yields by roughly 2–4 percentage points. This additional yield compensates investors for the unique risks associated with REIT investments—such as property market volatility, tenant credit risk, and economic cyclicality- compared to the relative safety of Treasuries. Over the long term, this yield spread has remained relatively stable, reflecting investors’ ongoing demand for compensation for the risks inherent in the real estate sector.

Financial articles from reputable sources like Bloomberg and Reuters have observed that the yield spread tends to widen during periods of market stress. In uncertain economic times, investors flock to U.S. Treasuries for safety, which drives their yields lower, while REIT dividend yields remain robust – or may even increase – to attract capital. This widening spread can indicate that REITs are undervalued relative to their risk profile, presenting a potential opportunity for future capital appreciation as market conditions stabilize.

Furthermore, academic research suggests that a wider yield spread might signal an undervalued REIT market. When REIT dividend yields are significantly higher than Treasury yields, investors demand a higher risk premium. This scenario may eventually lead to superior total returns for REITs as the market re-prices these assets, reinforcing the notion that REITs offer an attractive income premium relative to their inherent risks.

Growth

Real Estate Investment Trusts (REITs) offer investors an attractive avenue for growth by tapping into both secular trends and regional economic expansion.

REITs can capitalize on long-term sector trends. For instance, companies like WP Carey, STAG Industrial, and Vesta are well-positioned to benefit from the rising demand driven by nearshoring, the booming e-commerce logistics market, and strong industrial activity. Meanwhile, specialized REITs in healthcare and technology – such as ARE and Sila Realty Trust – stand to gain from ongoing, long-term shifts in demand within those sectors.

Beyond sector-specific trends, REITs also provide growth through regional focus. Patria, the largest REIT asset management firm in Latin America, exemplifies this by leveraging a diversified portfolio, robust cash flows in hard currencies, and strategic expansion into new markets. This localized approach enables REITs to position themselves in high-demand urban areas. However, it’s important to note that such growth can be influenced by local market conditions and regulatory environments.

Many REITs reinvest a portion of their cash flow to acquire additional properties. This reinvestment strategy increases their asset base and enhances future rental income and cash flow. A skilled management team can further boost growth by identifying and executing strategic acquisitions that add value over time.

In summary, REITs present a compelling, risk-adjusted opportunity for growth by leveraging both industry-specific trends and regional economic dynamics, while their reinvestment strategies and strategic management further enhance their potential to deliver sustainable income over the long term.

Risks

The biggest risk to REIT performance is not higher interest rates but rather economic downturns that negatively impact rents and occupancy. Over the past 30 years, the most prolonged negative REIT performance periods have occurred when 10-year Treasury yields were falling, rather than rising. This phenomenon is explained mainly by the collapse of Long-Term Capital Management (LTCM) and the default of Russian debt. Although interest rates declined during that period, credit conditions tightened significantly, making borrowing more expensive and less accessible for many asset classes, including commercial real estate. The collapse of LTCM and the Russian default led market participants to demand higher risk premiums, resulting in a reevaluation of leveraged REITs.

When liquidity evaporates and credit becomes scarce, REITs – relying on continuous refinancing and steady capital inflows – can suffer considerably due to restricted access to affordable financing. For example, during the LTCM crisis that began in October 1998, REITs experienced their most significant relative underperformance compared to other upcycles. Similarly, the subprime mortgage crisis, which started in late 2006, resulted in the lowest absolute returns for REITs since 1995. Research indicates that REITs tend to be the most risky during periods of rapid economic tightening, heightened market uncertainty, and stressed credit conditions.

Generally, REITs are most vulnerable during three types of periods:

- Rapid Interest Rate Increases: When borrowing costs surge, future cash flows are discounted at higher rates.

- Credit Crunches: When liquidity dries up, access to capital is severely restricted.

- Macro or Geopolitical Shocks: When unexpected external events trigger market panic and prompt a flight to safety.

Historically, REITs have rebounded strongly after such downturns, rewarding investors with both income and capital appreciation as risk premiums normalize.

Finally, when selecting a specific REIT, investors should verify that a REIT’s dividend is both sustainable and poised to grow. Since REITs must distribute 90% of their taxable income (which excludes depreciation), they often rely on funds from operations (FFO) to gauge true cash flow. A healthy REIT typically maintains a payout ratio of less than 80% of its cash flow. Additionally, caution is warranted against overleveraged portfolios. REITs should preferably have a leverage ratio below 6 – and against those showing a steady decline in cash flows or earnings, which may signal poor tenant performance, waning demand, or asset sales to cover debt.

Investors should target REITs with well-covered payout (below 80% of cash flow), low leverage (under 6x), and consistently growing rental income to ensure sustainable dividends.sh flow), low leverage (under 6x), and consistently growing rental income to ensure sustainable dividends.

Why now?

In the current climate – marked by temporary market pessimism, undervalued multiples, and strong long-term fundamentals – REITs present a compelling investment opportunity. The market’s excessive short-term focus has left many REIT properties undervalued, with large, blue-chip REITs trading at attractive discounts and even deeper discounts available among smaller, lesser-known players. A gravitational pull on valuations returns them to their long-term averages, which could positively impact mega-cap U.S. stocks.

Many REITs boast robust balance sheets with low leverage, with average loan-to-value ratios around 35%. Their debt is predominantly fixed and staggered over long-term maturities, reducing refinancing risks and interest rate sensitivity. Coupled with strong management teams that have a proven track record of delivering high returns on equity, these characteristics position REITs for secular growth and the ability to steadily increase rents over time.

Inflation, often seen as a headwind in other sectors, actually benefits REITs by increasing replacement costs and boosting rent prices, thereby enhancing the relative value of their assets. As the economy stabilizes and temporary headwinds fade, REITs are likely to see improvements in both dividend growth and capital appreciation, with cash flow yields and income growth opportunities recovering toward – and even surpassing – their historical averages.

The combination of discounted multiples, attractive yields, and strong balance sheets across various REIT sectors creates a persuasive investment case. With their defensive nature and attractive entry points relative to the broader equity market, reallocating capital toward REITs could yield robust income and significant upside as market conditions normalize.